Up to certain limits, it is possible to enjoy some savings income tax-free. The extent to which

this is possible depending on the rate at which you pay tax; not all routes are open to all.

Personal allowance

If you do not fully use your personal allowance elsewhere, any balance not otherwise used can

be set against your savings income, allowing it to be received tax-free.

Savings allowance

Basic and higher-rate taxpayers are entitled to a savings allowance. This is in addition to their

personal allowance.

For 2024/25, the savings allowance is set at £1,000 for basic rate taxpayers and at £500 for

higher rate taxpayers. The allowance is available in addition to the personal allowance and also

the dividend allowance.

Rising interest rates in recent years may mean that basic and higher rate taxpayers now receive

interest over their savings allowance on which tax is payable and which must be notified

to HMRC on their Self Assessment tax return. This may mean that they need to file a tax return

where previously they were not required to. Where this is the case, it is important to register

for Self Assessment.

Taxpayers who pay tax at the additional rate (which applies to taxable income more than

£125,140) do not benefit from a personal savings allowance and must pay tax on any savings

income unless it is otherwise exempt. They will also not receive a personal allowance, as the

personal allowance is fully abated at this level.

Savings starting rate

Savings income which falls within the savings starting rate band is taxed at the savings starting

rate of 0%. Depending on the individual’s personal circumstances, they may be able to enjoy up

to a further £5,000 of savings income tax-free.

The savings starting rate band is set at £5,000 but is reduced by any taxable non-savings

income. This is other taxable income over the personal allowance (but excluding any

dividends which are treated as the top slice of income). Consequently, the full £5,000 savings

starting rate band is available where other taxable income is less than the individual’s personal

allowance. The standard personal allowance is £12,570 for 2024/25. The savings starting rate is

eroded once taxable income over the personal allowance reaches £5,000.

The savings starting rate is applied before the personal savings allowance.

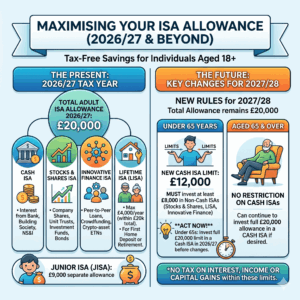

Tax-free savings accounts

If savings are held within a tax-free wrapper such as an Individual Savings Account (ISA), the

associated savings income is tax-free. A taxpayer can invest up to £20,000 in an ISA in 2024/25.

Maximum tax-free savings income

Where a person has the personal allowance available in full to set against their savings income,

they can enjoy tax-free interest in 2024/25 of £18,570 (personal allowance of £12,570 plus

savings starting rate band of £5,000 plus savings allowance of £1,000), plus that from tax-free

savings accounts.